Insurance costs can quietly eat into your monthly budget and for many households, premiums sneak up to over $1,000 per year on average just for auto insurance. Most people think these bills are fixed and that reductions only come from downgrading coverage. The truth is even small strategic tweaks and regular reviews could unlock hundreds in savings while preserving the protection you actually need.

Table of Contents

- Step 1: Assess Your Current Insurance Policies

- Step 2: Shop Around For Competitive Quotes

- Step 3: Implement Safety Measures And Technology

- Step 4: Increase Your Deductibles Strategically

- Step 5: Review And Update Your Coverage Regularly

Quick Summary

| Key Point | Explanation |

|---|---|

| 1. Assess your existing coverage | Review all your insurance documents to identify redundancies and potential savings opportunities. |

| 2. Shop for competitive quotes | Compare insurance quotes from multiple providers to find the best coverage at the lowest rate. |

| 3. Implement safety technologies | Utilize smart safety devices to demonstrate reduced risk and qualify for insurance discounts. |

| 4. Increase deductibles wisely | Raise your deductibles strategically to lower premiums, ensuring you can cover potential claims. |

| 5. Review policies annually | Regularly reassess your insurance coverage to adjust for life changes and optimize costs. |

Step 1: Assess Your Current Insurance Policies

Reducing insurance premiums starts with a comprehensive examination of your existing insurance coverage. This crucial first step allows you to understand your current financial protection landscape and identify potential areas for optimization. By carefully reviewing your policies, you can uncover opportunities to save money without compromising your essential protection.

Understanding Your Current Coverage Landscape

Begin by gathering all your current insurance documents. This includes policies for auto, home, life, health, and any specialized coverage you might have. Spread these documents out and create a comprehensive overview of your existing insurance portfolio. Pay special attention to the declaration pages, which outline your coverage limits, deductibles, and premium amounts.

As you review your policies, look for redundancies or overlapping coverages that might be unnecessarily increasing your total insurance expenses. According to the Insurance Information Institute, many consumers carry more insurance than they actually need, which directly impacts their premium costs.

Here is a checklist to guide you through the key areas to review in your existing insurance policies to identify savings opportunities and ensure proper coverage:

| Review Area | What to Look For | Potential Impact |

|---|---|---|

| Coverage Limits | Are they excessive for your actual assets? | Over-insurance increases costs |

| Redundant Policies | Any overlapping or duplicate coverage? | Eliminate unnecessary expenses |

| Deductible Amounts | Are your deductibles too low (higher premiums)? | Potential for lower premiums |

| Policy Bundling | Are you missing multi-policy discounts? | Savings on combined policies |

| Applicable Discounts | Not receiving discounts you qualify for? | Missed opportunities to save |

| Life or Lifestyle Changes | Recent changes impacting insurance needs? | Adjust for optimal protection |

Strategic Policy Assessment

Carefully evaluate each policy’s details. Check your current deductibles and consider whether they align with your financial situation. Higher deductibles typically result in lower monthly premiums. However, ensure you can comfortably cover the deductible amount in case of an emergency. Make a detailed comparison of your current coverage against your actual risk profile.

Key areas to scrutinize include:

- Coverage limits that might exceed your actual asset protection needs

- Bundling opportunities across different insurance types

- Potential discounts you might qualify for but are not currently receiving

- Age or lifestyle changes that could impact your insurance requirements

Document your findings meticulously. This assessment provides a clear roadmap for potential premium reductions and will serve as a foundation for your subsequent insurance optimization strategies. Remember, the goal is not just to reduce costs, but to maintain comprehensive and appropriate insurance protection tailored to your specific needs.

Step 2: Shop Around for Competitive Quotes

After assessing your current insurance policies, the next critical step in reducing your insurance premiums is actively shopping around for competitive quotes. This process involves strategically comparing rates from multiple insurance providers to identify the most cost-effective coverage that meets your specific needs.

Leveraging Digital and Personal Resources

Start by using online comparison tools and insurance quote websites that allow you to input your details and receive multiple quotes simultaneously. Digital platforms streamline the comparison process, saving you significant time and effort. Websites like Compare.com and similar insurance comparison sites can provide instant quotes from various providers, helping you quickly identify potential savings.

However, do not rely exclusively on digital platforms. Reach out directly to insurance agents who can provide personalized quotes and potentially uncover discounts that automated systems might miss. Independent insurance agents often have relationships with multiple carriers and can negotiate rates on your behalf.

Strategic Quote Gathering Approach

When requesting quotes, ensure you provide consistent and accurate information across all platforms. Minor variations in details can significantly impact quote prices. Prepare a comprehensive list of your current coverage, vehicle details, driving history, and personal information before beginning your quote search.

Key strategies for effective quote gathering include:

- Request quotes from at least 3-5 different insurance providers

- Ask about available discounts for bundling policies

- Inquire about potential savings for safe driving records

- Consider adjusting coverage levels to find optimal pricing

According to NerdWallet’s insurance research, consumers who actively compare quotes can save hundreds of dollars annually. The key is to be thorough, patient, and willing to negotiate.

Remember that the cheapest quote is not always the best option. Carefully evaluate each quote’s coverage levels, deductibles, and overall value. Your goal is to find a balance between affordable premiums and comprehensive protection that meets your specific needs.

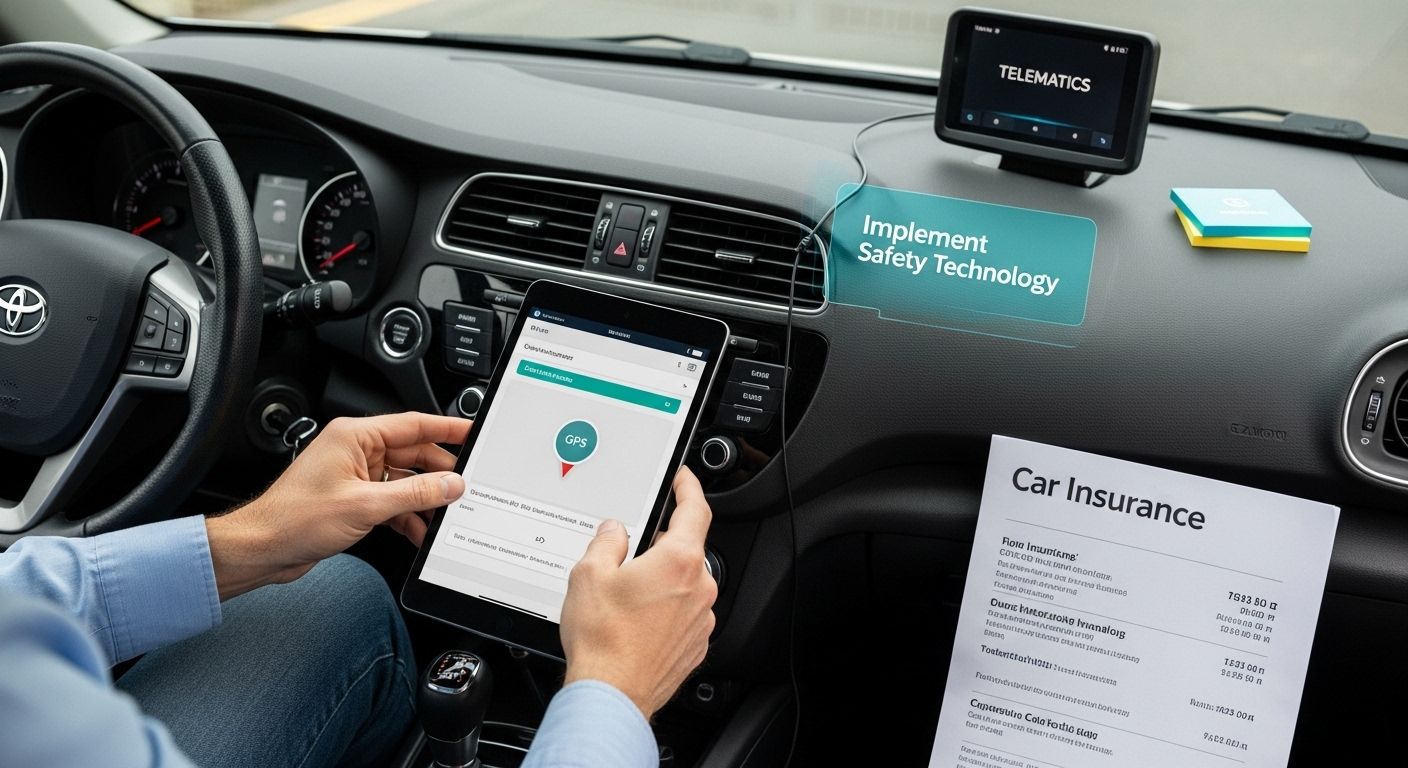

Step 3: Implement Safety Measures and Technology

Reducing insurance premiums isn’t just about comparing prices. Proactively implementing safety measures and leveraging modern technology can significantly lower your insurance costs. Insurance providers reward policyholders who demonstrate reduced risk through advanced safety technologies and preventative strategies.

Integrating Smart Safety Technologies

Modern technology offers numerous opportunities to minimize risk and signal responsible behavior to insurance providers. For vehicles, consider installing GPS tracking systems and advanced driver monitoring devices. These technologies provide insurers with concrete evidence of safe driving habits, potentially qualifying you for substantial discounts. Telematics devices that monitor driving speed, braking patterns, and total mileage can translate directly into lower premium rates.

Home insurance similarly benefits from technological interventions. Smart home security systems with integrated fire and burglar alarms, water leak detection, and remote monitoring capabilities demonstrate to insurers that you are actively protecting your property. Many insurance companies offer premium reductions of 5-20% for homes equipped with comprehensive security systems.

According to the U.S. Government Accountability Office, insurers are increasingly utilizing advanced technologies to assess and price risk more accurately. This means that investing in safety technologies is no longer just about protection but also about financial optimization.

Key safety technologies to consider include:

- GPS tracking devices for vehicles

- Advanced home security systems

- Smoke and carbon monoxide detectors

- Water leak detection sensors

- Smart locks and surveillance cameras

Beyond technological solutions, consider additional risk reduction strategies. For drivers, completing defensive driving courses can demonstrate responsibility and potentially unlock insurance discounts. Homeowners might reduce premiums by implementing storm-proofing measures, updating electrical systems, or improving home structural integrity.

To help you choose and implement effective safety upgrades, here is a summary of recommended technologies and actions, along with their insurance impact:

| Safety Upgrade | Insurance Type | Benefit/Discount Potential |

|---|---|---|

| GPS Tracking System | Auto | Lower risk, safe driving discounts |

| Telematics Device | Auto | Discounts for monitored driver behavior |

| Smart Home Security System | Home | 5-20% premium reduction |

| Smoke/CO Detectors | Home | Qualification for standard discounts |

| Water Leak Sensors | Home | Prevention, fewer claims, possible discounts |

| Defensive Driving Course | Auto | Eligibility for safe driver discount |

Remember that the goal is not just to install technology but to actively demonstrate reduced risk. Maintain documentation of your safety investments and proactively communicate these improvements to your insurance provider. Many insurers have specific programs and discount structures designed to reward policyholders who take measurable steps to minimize potential claims.

Step 4: Increase Your Deductibles Strategically

Strategically increasing your insurance deductibles is a powerful method to reduce your monthly premium costs. This approach requires careful financial planning and a clear understanding of your personal risk tolerance. By voluntarily choosing to pay more out of pocket in the event of a claim, you demonstrate to insurance providers that you are a lower-risk policyholder.

Understanding Deductible Mechanics

A deductible represents the amount you agree to pay before your insurance coverage begins. When you choose a higher deductible, insurance companies typically reward you with lower monthly premiums. The fundamental trade-off is between immediate monthly savings and potential out-of-pocket expenses during a claim. This strategy works best for individuals with stable financial reserves who can comfortably cover a higher unexpected expense.

Carefully assess your financial situation before making this decision. Calculate your emergency fund and determine how much you could realistically pay in case of an unexpected incident. For most insurance types like auto, home, and health, increasing deductibles from $250 to $1,000 can result in premium reductions of 10-25%.

According to the Insurance Information Institute, raising deductibles is one of the most direct methods to lower insurance costs. However, this strategy requires a nuanced approach tailored to your specific financial circumstances.

Key considerations when increasing deductibles include:

- Your current emergency fund balance

- Frequency of potential claims in your specific situation

- Risk of unexpected expenses in your personal or professional life

- Your comfort level with potential out-of-pocket costs

- The specific premium savings offered by your insurance provider

Consider creating a dedicated savings account specifically to cover potential higher deductibles. This approach provides a financial safety net and gives you the confidence to choose higher deductible levels. Some insurance providers even offer deductible reduction programs or rewards for claim-free periods, which can further optimize your long-term insurance expenses.

Remember that deductible increases should be incremental and carefully planned. Start with modest increases and monitor both your premium savings and your comfort level with potential out-of-pocket expenses. Regularly review and adjust your strategy as your financial situation evolves.

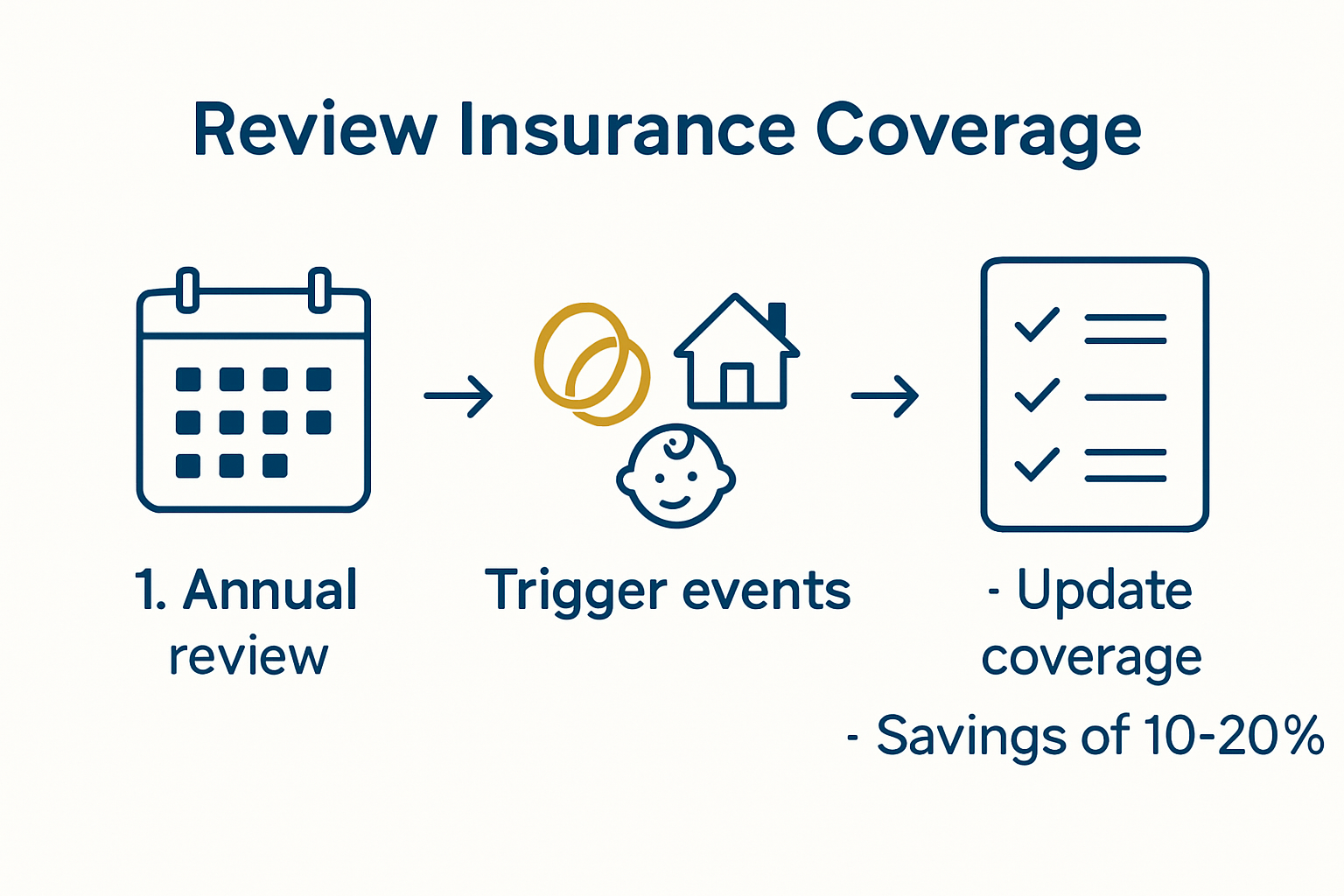

Step 5: Review and Update Your Coverage Regularly

Insurance is not a set-it-and-forget-it proposition. Regular review and strategic updates of your insurance coverage are crucial for maintaining optimal protection and managing costs. Life changes rapidly, and your insurance needs evolve correspondingly, making periodic reassessment a financial imperative.

Creating a Systematic Review Process

Establish a structured approach to reviewing your insurance policies at least annually. Mark your calendar with a specific date each year dedicated to comprehensive insurance evaluation. This proactive method ensures you never overlook critical changes in your personal circumstances that might impact your coverage needs.

Life transitions such as marriage, having children, purchasing a home, changing jobs, or experiencing significant income shifts can dramatically alter your insurance requirements. Each major life event presents an opportunity to optimize your coverage and potentially reduce premiums. For instance, becoming a homeowner might qualify you for new bundling discounts, while having a child could influence your life insurance needs.

According to NerdWallet’s insurance research, consumers who regularly review their policies can save an average of 15-20% on their total insurance expenses. This significant potential savings makes the review process not just prudent but financially strategic.

Key elements to examine during your annual insurance review include:

- Changes in your personal and professional life status

- Significant asset acquisitions or disposals

- Shifts in your financial stability and income

- Emerging insurance products and coverage options

- Potential new discounts or bundling opportunities

Utilize digital tools and insurance comparison platforms to streamline your review process. Many online resources provide comprehensive analysis tools that can help you quickly identify potential savings and coverage gaps. Consider scheduling consultations with independent insurance agents who can offer personalized insights into your specific situation.

Do not view this review as a tedious task, but as a strategic financial planning opportunity. Approach your insurance review with the same diligence you would apply to managing investments or reviewing your annual budget. Each review is a chance to ensure your insurance portfolio remains aligned with your current life circumstances, providing optimal protection at the most competitive rates.

Unlock Vehicle Savings with Dupno’s GPS Solutions

Are you trying to lower your insurance premiums but still worried about vehicle risks? The article highlighted how safety technology and smart risk reduction can have a direct impact on your insurance costs. Many readers feel the pain of high insurance expenses, uncertain coverage, and not knowing if they qualify for discounts. By implementing advanced safety measures, you not only protect your assets but also demonstrate to insurers that you are a responsible owner, leading to better rates.

Now is the time to take control. Enhance your vehicle security and operational efficiency with Dupno’s GPS vehicle tracking systems and make your insurance profile more attractive. With real-time tracking, driver behavior analysis, and proactive theft protection, you can reduce risks and meet the requirements outlined in the article for potential premium discounts. Visit Dupno.com today to discover how our technology and support can help you achieve real savings and greater peace of mind. Start your journey toward lower insurance premiums now with the proven leader in vehicle management.

Frequently Asked Questions

How can I assess my current insurance policies to save money?

Start by gathering all your insurance documents and creating an overview of your coverage. Pay attention to declaration pages for coverage limits, deductibles, and premium amounts, then look for redundancies or overlaps in your policies that could lead to cost savings.

What strategies can I use to find competitive insurance quotes?

Utilize online comparison tools and ensure you provide consistent information across different platforms. Contact insurance agents for personalized quotes and inquire about available discounts for bundling policies and safe driving records.

What safety measures can I take to reduce my insurance premiums?

Implement smart technologies like GPS tracking for vehicles and comprehensive home security systems. These technologies show insurers that you are taking proactive steps to minimize risk, which can lead to significant discounts on your premiums.

How often should I review my insurance coverage?

It’s advisable to review your insurance policies at least once a year. Key life events such as marriage, the birth of a child, or purchasing a home can affect your coverage needs, potentially leading to opportunities for cost savings or necessary adjustments.

Recommended

- Loyalty Offer for Dupno GPS Tracker Users

- Fleet Expense Management: Save Costs and Boost Efficiency

- Top Benefits of Fleet Tracking for Businesses in 2025

- Top Benefits of Fleet Tracking for Businesses in 2025 | GPS Tracking Service – Dupno Tracker | Best Vehicle Tracking in Bangladesh %

- How to Lower Premiums: Easy Steps for Car and Home Owners 2025 – Savvy Insurance